A strong M&A position comes from marketing the right numbers for your IT services company.

IT services continue to be one of the hottest M&A sectors in the market. It’s a trend that has remained steady for the past couple of years–almost every week, we hear from another private equity (PE) firm looking for high-quality acquisition opportunities in IT Services

Factors driving this trend include:

- Industry leaders like Microsoft converting to subscription-based services, familiarizing customers with recurring-fee models.

- Increasing complexity in IT systems, creating a scarcity of qualified talent–and a ripe opportunity for outsourced managed services.

- Evolving cybersecurity needs make risk management a top priority for businesses of all sizes. Modern security risks present unique challenges for businesses to stay protected–and prepared.

These tailwinds have driven the need for all types of businesses to be equipped with specialized IT support, accelerating growth trends in the industry. This growth has been accompanied by a very sticky recurring revenue model.

These factors create a dream hunting ground for PE firms. And with so many firms eager for opportunities–it’s a seller’s market (and you might be selling yourself short).

What PE-Interest Means for Sellers

Typically, many IT services business owners use a simple heuristic to value their business. Most often, it’s EBITDA, or earnings before interest, taxes, depreciation, and amortization. But is that really the most accurate metric?

Here’s why business owners tend to rely on EBITDA. Generally speaking, larger companies with a higher EBITDA garner a higher multiple. And platforms–acquisitions that the PE will use as the nexus of their roll-up acquisition strategy, receive a premium.

The reality is that valuation is much more nuanced. Even for two similar companies with the same EBITDA, one could be valued at a significant premium over the other.

Embarc is in a unique position where many of our team members come from Private Equity and have intimate knowledge of the inner workings of how PE firms evaluate investment opportunities.

We want to provide business owners and operators with timely advice they can use today to prepare their businesses for sale down the road–in the next several years. When it comes to M&A, it’s not just about growing EBITDA; how you grow it makes a big difference in the end result.

Here we share the Top 8 metrics that we have found most valuable when an IT services company goes to market to sell itself.

The Top 8 Metrics for IT Services Companies

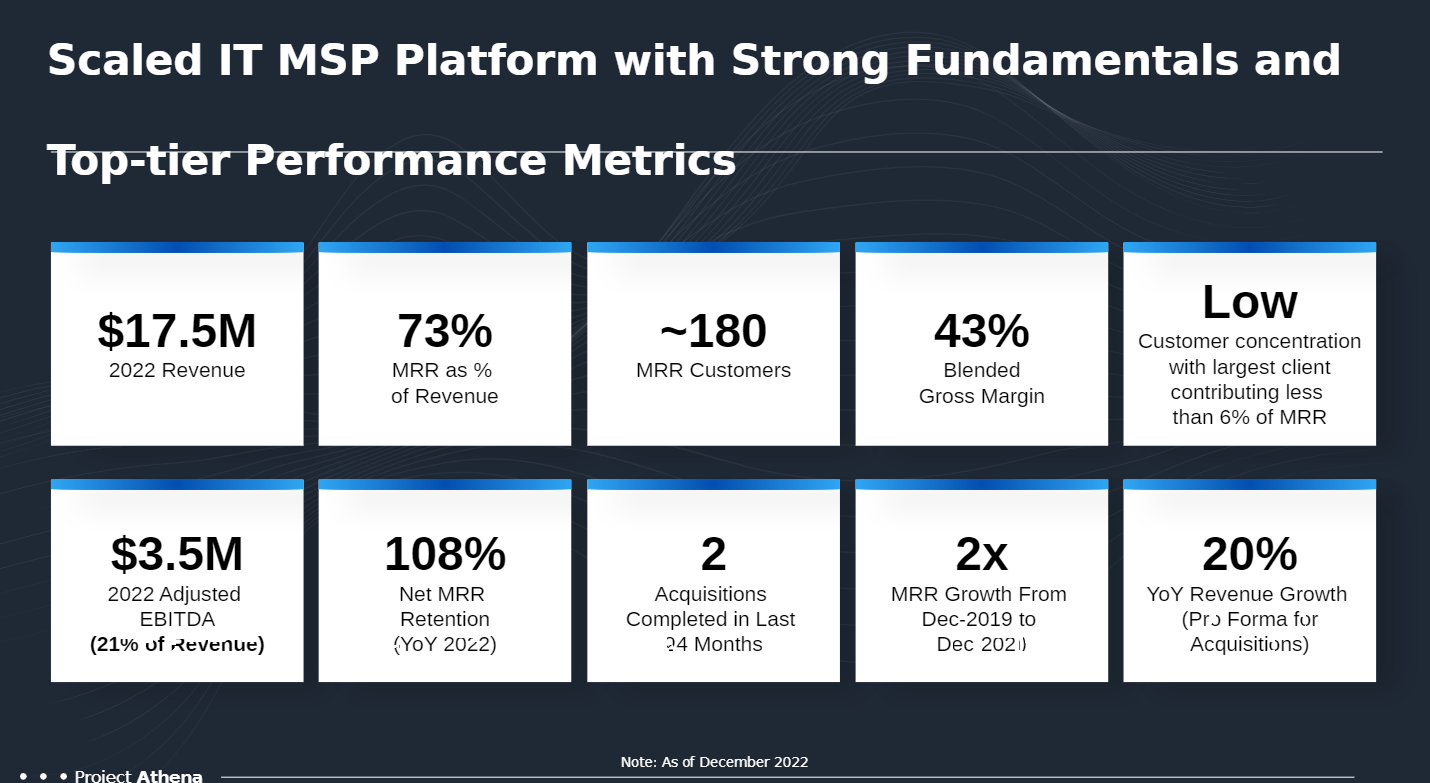

When we market an opportunity, our first page is typically similar to this, where we highlight the Top 8 Metrics

1. Revenue Growth

Revenue growth is one of the most important metrics. Growth drives multiples. It is consistent across industries, from IT services to industrial companies or retail services. This metric provides a general pattern that communicates growth in relation to future potential. Practically speaking, buyers value what is possible in the future–not what has been achieved in the past.

An above-average or above-market growth rate also demonstrates that the company has a strong market position, is gaining market share, and has potential for future growth. Needless to say, this makes the company an attractive acquisition target for buyers looking to expand their revenue and market share.

But growth isn’t the only way to communicate value.

2. Percent of Revenue that is Recurring

The percentage of revenue that is recurring refers to the portion of a company’s revenue that is generated from ongoing contracts or agreements that are renewed or extended periodically. This revenue is considered “recurring” because it is expected to continue for an extended period of time rather than being a one-time sale.

This type of stability is another factor that drives higher multiples. It’s why pipelines and utilities trade at such high multiples despite their relatively low growth.

Companies with a higher percentage of recurring revenue are considered to be more stable and, therefore, more valuable in an M&A deal. The predictability of recurring revenue provides more confidence in future value.

In M&A, it’s important to separate recurring revenue like ongoing contracts for managed IT services from one-time or limited-delivery services like a specific custom development or technology infrastructure project. It’s also worth noting that re-occurring revenue, even if it’s not derived from a true subscription, is valued at a premium.

3. Customer Retention Rate

Another very important stability metric is the customer retention rate. This number is a measure of how many customers stick with a company over a period of time. In IT services, a high customer retention rate can indicate value because it signals that the company is providing quality services at an appropriate price. In other words, an IT service provider’s customer retention rate indicates how sustainable the business model is and whether or not it is positioned for future growth.

In M&A, combined with the recurring nature of the revenue stream, a high customer retention rate further solidifies the certainty of future value potential.

4. Net Dollar Retention Rate

Still, customer retention rates only tell part of the story. Another important metric in M&A is the net dollar retention rate which factors in retention, expansion, and churn over time to provide a more comprehensive view of the dollar value of a customer in terms of revenue generated from both ongoing services or upsells.

This metric is a combination of growth and stability. A high net dollar retention rate shows the company has a strong account management capability and is able to cross-sell or up-sell additional products, thereby creating growth within existing customers.

Even if a company has a somewhat low retention rate, a high net dollar retention rate can more than compensate for that shortcoming.

5. Gross Margin by Service/Product

Gross margin measures the profitability of a specific service or product. It is important to analyze the gross margin by product and service line.

For example, for a typical IT managed services company, we would want to see gross margin by:

1. Managed Services/Help Desk Services

2. Cybersecurity

3. Product Resale (e.g., Microsoft 365)

The Gross Margin by Service metric would indicate how profitable each of those three services is compared to the industry average.

Here is why this number is important. Operating expenses typically grow less than the topline and will expand the margin as the company grows. However, gross margin is often consistent unless specific action is taken e.g., price increase or labor cost restructuring.

In M&A, this metric is an indication of the mid-to-long-term value-creation capability of the company.

.

6. Adjusted EBITDA

Yes, EBITDA is still important. It’s just not the only important metric. Adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a financial metric that is commonly used in mergers and acquisitions (M&A) to assess the profitability of a company. While it’s not a standard accounting measure, meaning that there are different ways of calculating EBITDA, it is a common proxy as a valuation metric.

EBITDA is a measure of a company’s operating performance and is calculated by taking the company’s earnings before interest, taxes, depreciation, and amortization and adjusting for certain non-operating expenses, one-time charges, and other factors. In effect, it serves as a rough proxy for cash flow, excluding capital expenditures.

The purpose of adjusting EBITDA is to illustrate what the company’s performance looks like on a normalized basis or what it would be like under private equity ownership. Some common adjustments include:

- Expenses Related to Stock-Based Compensation

- Owner Expenses

- Restructuring Charges

- Other Non-Recurring/One-Time Expenses

7. Customer Concentration

The customer concentration metric shows the dollar amount of revenue generated by a customer group. This measurement indicates the extent to which a small group of customers impacts the total revenue. Generally, in M&A, this can point to unique risk factors that might make the deal more or less attractive to a buyer.

When a company is dependent on a small group of customers, the risk of financial impact from losing a customer is greater. For example, if a technology company is acquiring an IT service provider in order to gain access to specific large-volume clients, they need to understand the associated risks of losing one of those clients during integration. In this respect, customer concentration can either encourage or discourage a deal based on the strategic perspective.

Many startups or founder-owned businesses see some level of customer concentration because that customer was the anchor tenant that enabled the company during its infancy. There are many ways to articulate the mitigation of the customer concentration risk, and there should be a targeted narrative to address this.

8. Customer Tenure

Customer tenure is a loyalty metric that indicates how long a customer tends to stay with the company. Long-term, satisfied customers are a key driver of growth and are generally considered a positive in M&A. This is also a measure that may help mitigate the aforementioned customer concentration risk.

Happy, loyal customers are more likely to stay with a company through changes and even more likely to recommend that company, generating future growth. In M&A, a good customer tenure track record indicates stability, strength, and value.

It’s important to note that the IT services industry is centered around providing long-term, mission-critical services. Problems with tenure (also expressed as a high customer churn rate) drive up customer acquisition costs making it more expensive to market the products or services that the company offers.

On a deeper level, poor customer tenure rates might also indicate service quality or delivery problems, low trust levels, or ineffective marketing strategies.

For fast-growing companies, the average tenure may be short due to continued new customer onboarding in recent years. In this instance, combining tenure with a cohort-based retention analysis can be a powerful way to emphasize both strengths.

Expressing Value in an M&A Deal

Whether you are on the buy side or the sell side–communicating value is going to be the primary focus in closing a deal. Sellers who are better prepared to demonstrate their value by showing potential buyers that they have a sticky revenue base with robust growth supported by long-standing, loyal customers and a profitable business model will get more offers with more attractive terms than those who fail to communicate their value.

A qualified advisory team can help you identify and build a highly compelling narrative that accentuates the unique value of your specific business, bringing the best offers to the table.

When Embarc Advisors led its first IT services sell-side process, we received over 50 interested parties and nearly a dozen conforming/qualified IOI bids without even disclosing the company name or meeting the management team. This was possible because we provided the key ingredients for each buyer to underwrite the value of the company.

For owners and management teams that are not looking to sell in the immediate term, these metrics still have an important implication. The first thing that private equity does when they acquire a company is to install a CFO. This is so that they can monitor these key metrics and provide strategic input into optimizing these metrics – driving value creation for the company. A strategic finance-oriented CFO team can help IT services firms to reap some of that benefit before a transaction and therefore maximize their value at the time of the sale.

Reach out to Embarc Advisors if you want to learn more about how you can maximize your value, whether it is for the medium term or the short term.

Or, learn more about the value we can offer through a new approach to corporate development for SMBs.